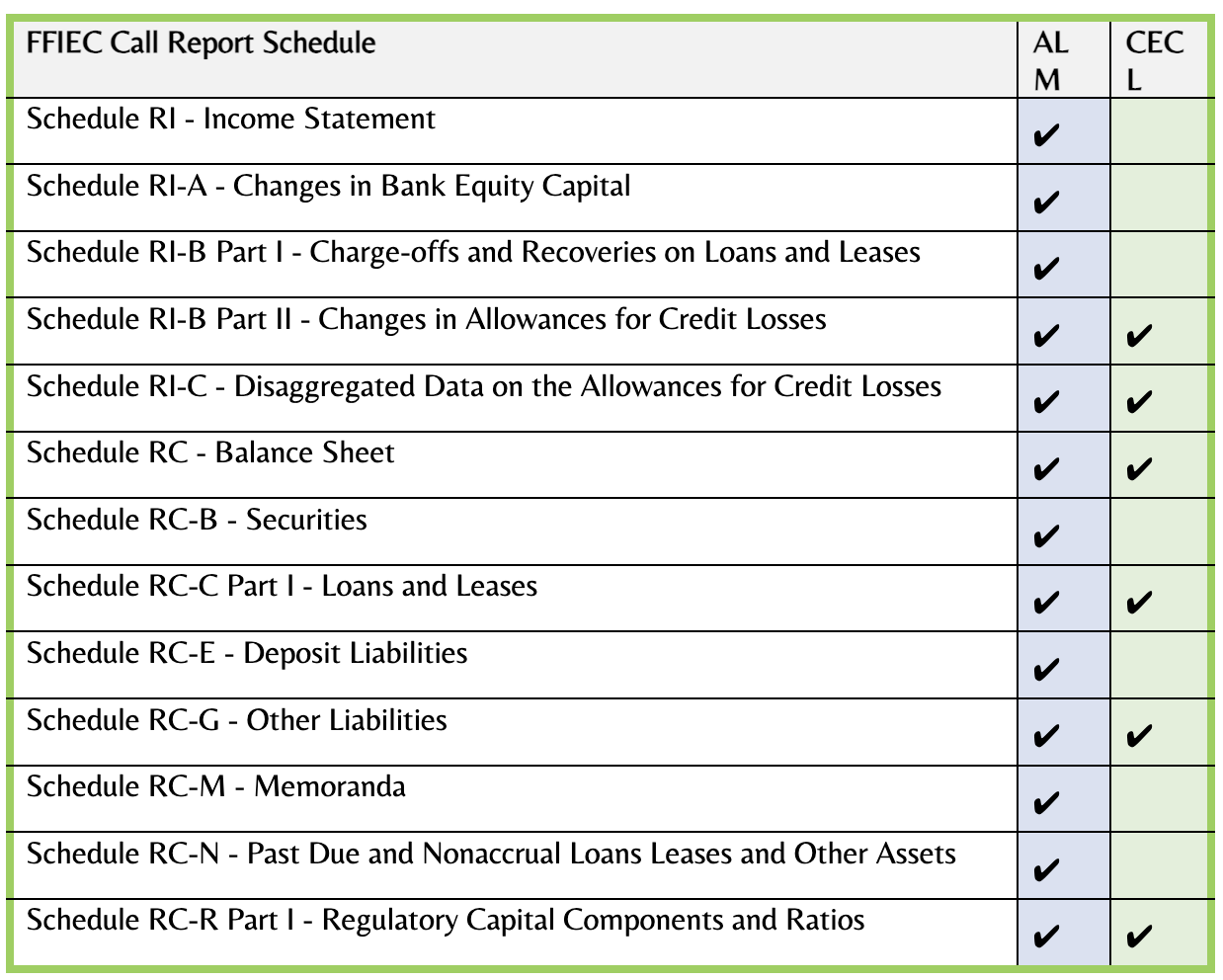

Community banks can gain a competitive edge by employing model validation of their regulatory reporting models. Banks submit quarterly Federal Financial Institutions Examination Council (FFIEC) Call Reports that detail an institution’s business and financial health. These reports mainly employ Asset Liability Management (ALM) and Current Expected Credit Loss (CECL) model outputs. The table lists the key sections of the Call Report and the model outputs

employed in each section. When these models produce incorrect outputs or are misused—whether from flawed assumptions, poor data, inappropriate application, software bugs, or governance failures—the consequences can be broad, severe, and sometimes irreversible.

ALM models inform gap analysis, hedging decisions, pricing of deposits and loans, and capital allocation. Incorrect assumptions about deposit decay, prepayment rates, interest rate paths, or re-pricing behavior can produce misleading net interest income (NII) and economic value of equity (EVE) projections. A bank that overestimates deposit stickiness or underestimates rate sensitivity may under-hedge and suffer large NII declines or mark-to-market losses when rates move. Conversely, unnecessary hedging based on faulty signals can incur hedging costs that squeeze margins. Mispricing of products from erroneous ALM outputs can yield unprofitable originations, adverse selection, and competitive disadvantage. Persistent mismanagement of ALM can erode capital, provoke covenant breaches, and, if unrecognized, culminate in rapid liquidity stress or insolvency during a market shock.

CECL models estimate lifetime expected credit losses and drive loan loss allowances, provisioning, and earnings volatility. If CECL inputs or model structure are wrong—e.g., inaccurate historical loss data, mis-specified macroeconomic forecasts, or incorrect segmentation—the bank can materially understate or overstate reserves. Under-reserving leads to an inability to absorb actual credit losses, eroding earnings, capital, and solvency during stress. That can trigger regulatory enforcement, forced capital raises, or, in extreme cases, closure. Over-reserving artificially depresses earnings, undermines market confidence, reduces lending capacity, and may create unwarranted reputational damage or shareholder dissatisfaction. Both scenarios impair capital planning, misguide management’s underwriting and pricing decisions, and can mask emerging portfolio deterioration until losses crystallize.

Model validation facilitates top tier ALM and CECL modeling so a community bank can deliver exceptional value to its customers and shareholders as well as satisfy regulatory requirements. Secure strategic edge by engaging Martingale Solution Group for ALM and CECL model validation. Contact Martingale Solution Group for a consultation.